Crypto-Backed Loans: Deep Insights

Crypto-backed loans will become a very serious financial instrument, and not a niche experiment, in a market where timing is everything and volatility is the order of the day. This guide helps to understand the true way crypto-backed loans work, where the risks are disguised and how individuals can exploit them without the need to sell their online assets in a strategic manner.

The Fascination behind Crypto-backed Loans

The existence of crypto-backed loans is due to the fact that the owners of digital assets require funds without leaving the market. Within ten years, they have turned experimental blockchain products into multi-billion-dollar lending systems that traders and investors use, as well as casino and iGaming players.

The History Of Lending: Pawnshops Into Blockchain

The conventional loans are based on credit score and intermediaries. The crypto lending substitutes the trust with the collateral and code:

No credit checks

Assets substitute the income verification.

Enforcement is carried out through smart contracts.

This reflects the traditional asset-backed lending but without permission across the world.

Why Liquidity Matters In Volatile Markets

Liquidity allows users to:

Cover short-term expenses

Fund casino bankrolls without selling BTC or ETH

When the market is down, do not engage in emotional selling.

Liquidity is a component of bankroll discipline, not speculation, to gamblers and traders.

Comparison: Crypto Loans As Digital Pawnbroking

Crypto pawnshop lending functions as an international pawnshop:

Lock your asset (BTC, ETH, stablecoins)

Receive liquidity

Get the property back upon payment.

The most important distinction: openness, automation and 24/7 accessibility.

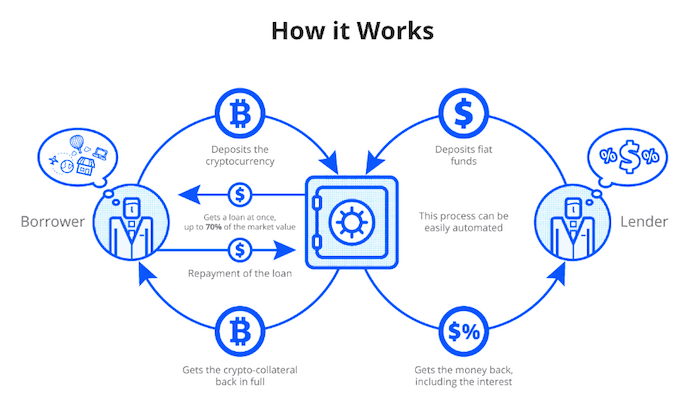

How It Works

The crypto-backed loans are based on overcollateralization to handle the volatility risk. The value of the loan received by the borrowers exceeds what they deposit in the form of crypto.

A default on the prescribed collateral leads to either margin call or automatic liquidation.

Loan To Value (Ltv) Ratios In Detail

Asset | Typical LTV | Borrowing Power |

BTC | 40–50% | $5,000 on $10,000 BTC |

ETH | 45–55% | A little bit more so due to liquidity |

Stablecoins | 80–90% | Lower volatility risk |

NFTs | 20–40% | Illiquid, higher risk |

Lower LTV means safer loans but less liquidity.

More than Credit Access Benefits

Tax Efficiency: Borrowing Vs Selling Crypto

Sales of crypto attract capital gains tax in most regions. Borrowing does not- crypto loans are popular forms of tax-deferral (professional advice required).

Privacy and accessibility

No credit checks

Minimal personal data

Global access

This renders crypto lending to be available where conventional banking is unavailable.

Casino & Igaming Use Case

Casino customers apply to lending partners to:

Retain long term assets.

Independent bankroll of investments.

Respond fast to bonuses or volatility.

Professional Advice On How To Find The Right Platform

Security signals

Independent audits

Insurance coverage

Cold storage custody

Interest rates & hidden costs

Always review:

Liquidation penalties

Withdrawal fees

Variable-rate mechanics

User experience

Mobile alerts, real-time LTV tracking, and clear dashboards are essential—especially for volatile assets.

Conclusion

Crypto-backed loans are at a middle position between long-term crypto and liquidity urgency. Utilized wisely, they allow you to check the wallet without having to sell at the inopportune time. Wasted recklessly, they may increase the losses as much as profits. It is necessary to understand loan-to-value, liquidation conditions, and the reputation of the lending site before pledging to an amount of loan.